What is the EN 16931 standard?

This article was last updated on 11 November 2025 to reflect the formal approval and B2B-specific details of the updated EN 16931-1:2025 e-invoicing standard.

E-invoicing standards are like a common language for business. They ensure that electronic invoices (e-invoices), whether sent from a supplier in one country or received by a buyer in another, can be transmitted and processed smoothly. By specifying how invoices must be structured and formatted, standards such as EN 16931 enable different accounting and ERP systems to “talk to each other”, thereby ensuring compliance, security, and interoperability between trading partners.

What is the EN 16931 standard?

The EN 16931 standard is a European norm that defines the technical specifications for the content and format of electronic invoices. Initially established by the European Committee for Standardisation (CEN) in 2017 as EN 16931-1:2017, the standard was primarily intended for business-to-government (B2G) transactions. Since then, the standard has evolved and been updated. Recently, the CEN has approved an updated semantic standard, EN 16931-1:2025, adapted specifically for business-to-business (B2B) transactions. It supports the new Digital Reporting Requirements (DRR) under ViDA and will supersede the 2017 version. It is expected to be published by May 2026.

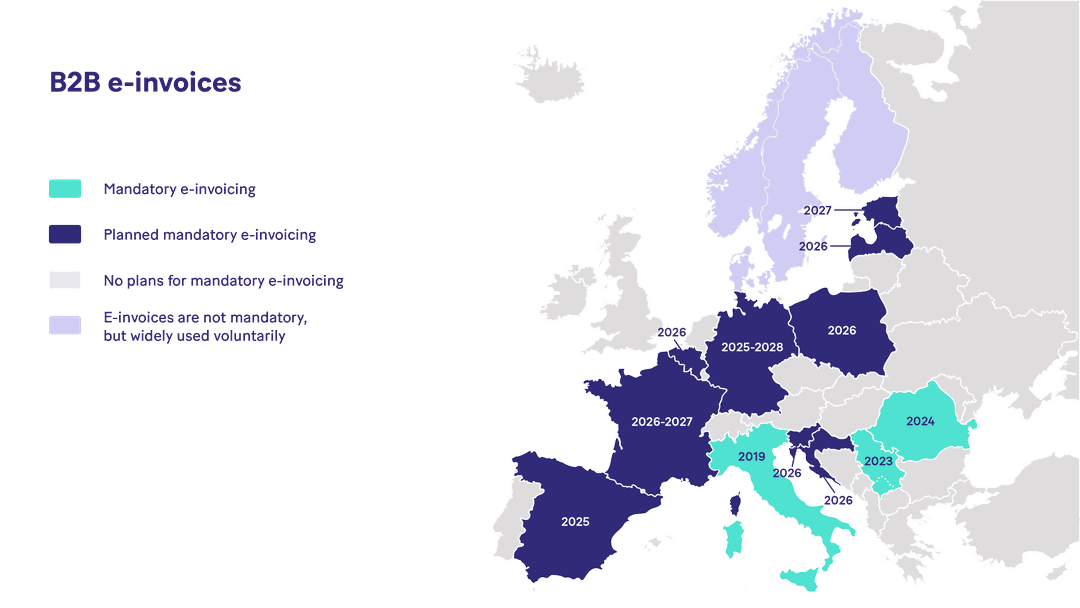

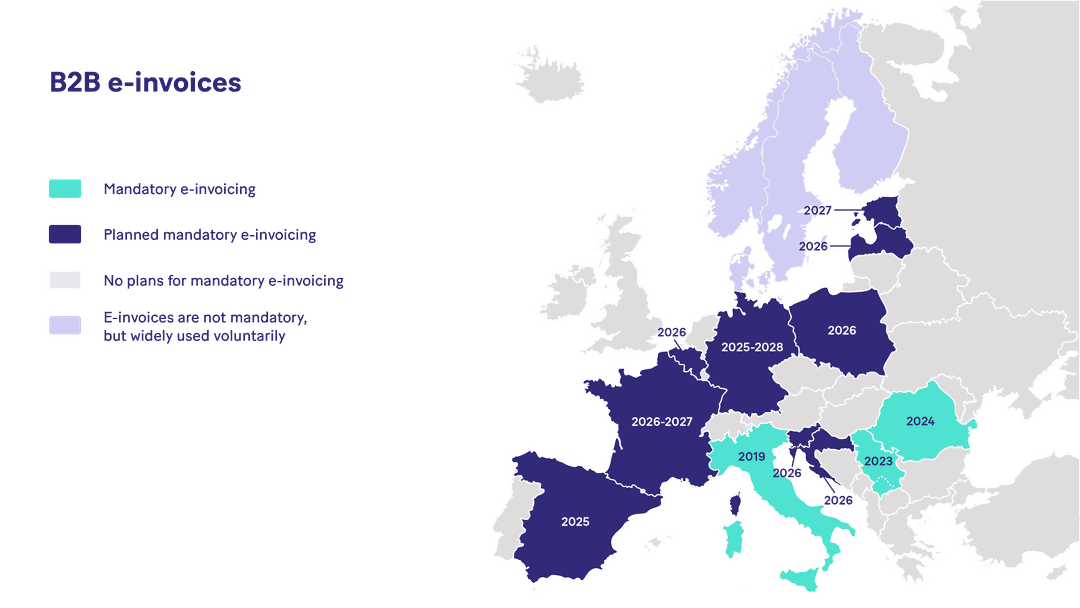

The aim of the standard is to harmonise electronic invoicing (e-invoicing) across the European Union, meaning that Member States have a standardised format, implementation and specification criteria to adhere to. By harmonising the format of electronic invoices and their implementation process, Member States can easily facilitate cross-border trade and transactions. Furthermore, the standard will become mandatory for all intra-Community B2B transactions starting 1 July 2030.

What are the compliance levels for the EN 16931 standard?

The European Commission details three areas that make up the EN 16931 standard, each crucial for ensuring seamless e-invoice exchange within the EU:

The invoice document

The implementation

The specification

The invoice document

In order to be considered compliant under the standard, the electronic invoice document must adhere to the rules defined for the CORE invoice or the CIUS (Core Invoice Usage Specifications) specification on which it is based.

"CORE" represents the core invoice data model defined in the European Norm (EN) 16931-1. It encompasses the essential elements of an invoice and provides a syntax-independent framework for defining invoice requirements.

"CIUS" stands for Core Invoice Usage Specification, which is an extension of the core invoice data model. CIUS further defines and refines the invoicing norm base, allowing for additional data elements and specifications beyond the core model. For example, each EU Member State can define its own CIUS to address specific legal, regulatory, and business requirements not covered by the core standard, such as tax reporting or public procurement. Examples of these national CIUS or compliant local formats include Fattura PA in Italy, XRechnung in Germany, and Factur-X in France.

This means that the electronic invoice must contain all mandatory information, it must be structured as specified, the amounts must be calculated as specified, and the invoice’s elements must only contain allowed values, such as codes.

The implementation

The European Commission details two aspects within the implementation criteria.

Firstly, a compliant receiver of an electronic invoice must accept and process all invoices that conform to the European e-invoicing standard CORE data model or a CIUS. This ensures that any optional information included by the sender, as allowed by the CORE or relevant CIUS, will be properly processed and not rejected.

Secondly, a compliant sender must be able to generate electronic invoices that adhere to the European e-invoicing standard or a CIUS.

The CIUS that a specific sender or receiver must or can use may be restricted by the EU Member State where they are registered, through the Member State's legal adoption of Directive 2014/55 on electronic invoicing in public procurement.

The specification

When an invoice document and its implementation are based on a CIUS, that CIUS must meet the criteria in section 4.4.2 of EN 16931 part 1. In essence, a CIUS must be a legal and compliant subset of the CORE model. This ensures that any system capable of receiving and processing the full CORE standard can also read a compliant CIUS. However, a system only configured for a specific CIUS may not be able to process the full, broader CORE standard or a different CIUS.

Key updates to the European Standard EN 16931-1:2025 for B2B

The revised semantic standard EN 16931-1:2025 introduces specific changes to accommodate B2B transactions and the ViDA Digital Reporting proposals. These include:

New invoice data: Provisions for adding bank IBAN details, mentioning the use of triangulation simplification (where relevant), and incorporating corrective invoice sequential numbering.

Transaction support: Enhancements for facilitating repeat and multiple orders, adding discounts on early payments/late fines, and managing FX (Foreign Exchange) information.

VAT schemes: Inclusion of a wider range of exempt supplies and support for national special VAT schemes (e.g., margin scheme).

What are the benefits of adopting the EN 16931 standard?

One single standard creates simpler interoperability, validity, and integrity of electronic invoices, facilitating cross-border trade by ensuring that e-invoices comply with the same requirements across EU Member States. By adhering to one format, businesses within the European Member States can significantly reduce processing errors, which in turn creates faster payment cycles and greater operational efficiency. One standard means one processing format, which allows businesses to easily feed the electronic invoices into their accounting systems and ERP platforms for further processing and payment, reducing the need for manual intervention and the risk of data entry errors.

Even though the EN 16931 standard has clear benefits, the standard still has variations used across the Member States.

The use of the EN 16931 standard

The EN 16931 standard can be implemented using the Universal Business Language (UBL) or Cross-Industry Invoice (CII) formats, as well as local formats (CIUS) such as FatturaPA in Italy or Factur-X in France. Compliant formats are designed to meet the criteria set out in the standard and enable businesses to generate and exchange compliant electronic invoices seamlessly.

But why do variations exist?

The EN 16931 standard facilitates the use of different syntaxes. The standard acts as a guideline to ensure that certain formatting, implementation, and specification criteria are met, but then allows flexibility for Member States to tailor the standard to fit their national needs, such as different taxation aspects, business needs, and technological capabilities. Here are some of the more commonly used formats:

Core compliant formats (UBL/CII): Universal Business Language (UBL) and Cross-Industry Invoice (CII) formats are the primary syntaxes used to implement the EN 16931 CORE data model.

National CIUS/local formats: These are country-specific implementations based on and compliant with the EN 16931 standard, such as:

Factur-X (identical to its German equivalent, formerly known as ZUGFeRD): Factur-X is a hybrid electronic invoice format that combines both human-readable PDF and structured XML data in a single document. This format ensures that invoices are both visually appealing and machine-readable, improving efficiency and compliance with e-invoicing standards.

FatturaPA: is the official format for electronic invoices in Italy, specifically designed for transactions involving public administrations and, later, extended to all business-to-business (B2B) and business-to-consumer (B2C) transactions. It is an XML-based format and includes a predefined set of data elements, ensuring consistency and compliance with Italian regulations.

CIUS-PT: The national e-invoicing implementation in Portugal, which adheres to the EN 16931 standard for use in public procurement.

Other local formats: In addition to the example provided above, companies can also use local or industry-specific formats tailored to their operational needs. These formats may be based on regional regulations, industry standards or specific business requirements.

By offering a variety of formats for implementing the EN 16931 standard, businesses have the flexibility to choose the most suitable option based on their internal systems, trading partners' preferences, and compliance requirements. Exploring these variations can help organisations streamline their invoicing processes and ensure seamless interoperability with partners across different sectors and regions.

Understand even more about electronic invoicing

Understanding electronic invoicing can be a complex task, which is why at Banqup, we make it simpler for you.

Explore our compliant e-invoicing solution today and connect with our local team to learn more. To receive updates on mandates and industry shifts in a more timely manner, follow us on LinkedIn.