Slovenia makes progress with future e-invoicing and e-reporting obligations

Last updated on 30 October 2025, to reflect the final enactment of the e-invoicing law, postponing the mandate to January 2028 and removing the e-reporting requirement.

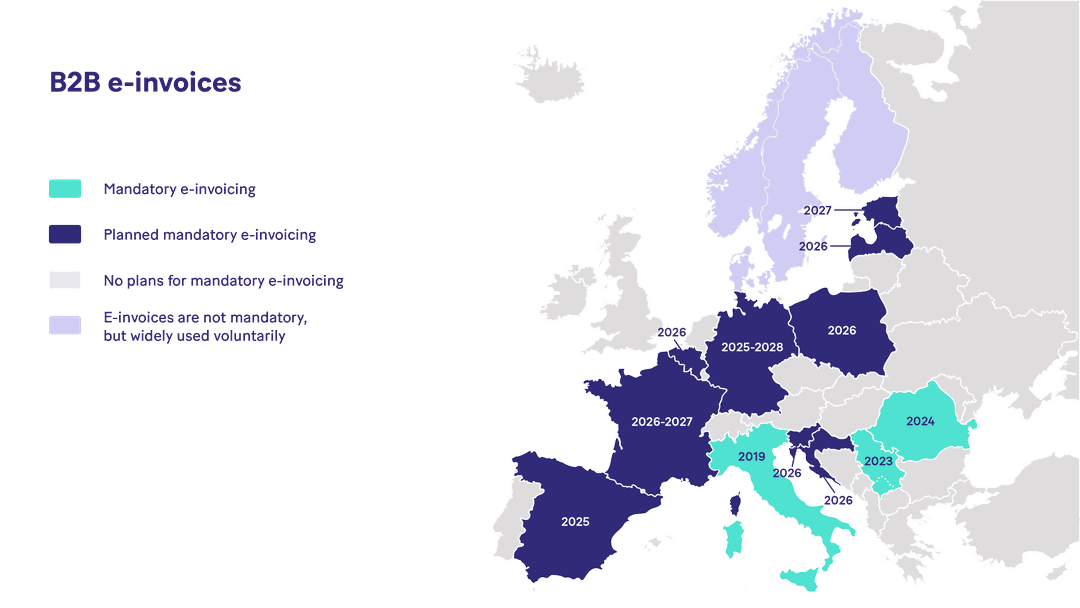

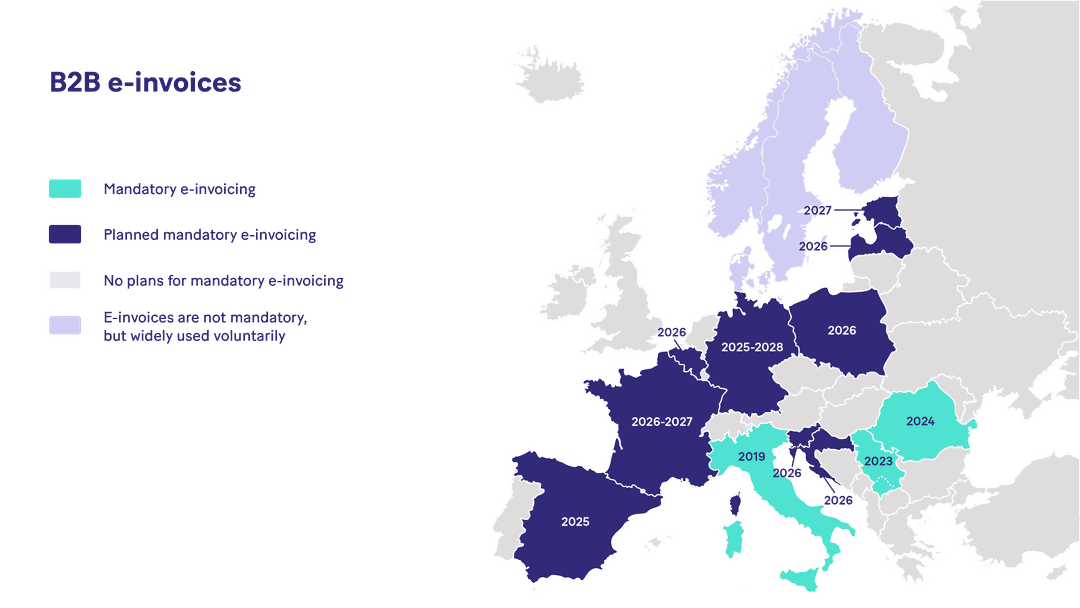

Slovenia sets its sights on mandatory e-invoicing by 2028, aligning with a growing trend in Europe's digital tax landscape, while definitively removing the requirement for e-reporting.

In late July 2024, Slovenia took its first steps towards introducing mandatory electronic invoicing and electronic reporting for businesses in their commercial activities by submitting a proposal for the obligation to use e-invoicing and e-reporting. Having analysed the results and obligations in other European countries, including Italy, Romania, Poland, and Belgium, Slovenia opted for the Decentralised Continuous Control and Exchange Model (DCTCE).

The initial legislative framework, as outlined in the Draft Law on the Exchange of Electronic Invoices and Other Electronic Documents (ZIERDED) published by the Ministry of Finance on 11 February 2025, had set the initial target date as 1 January 2027. This was a postponement from earlier proposals of April and July 2026, and the law had already abandoned the idea of mandatory real-time reporting.

However, this has been superseded: on 23 October 2025, Slovenia’s National Assembly officially adopted the new Act on the Exchange of Electronic Invoices and Other Electronic Documents. This establishes 1 January 2028 as the definitive roll-out date for the B2B e-invoicing mandate, which is a further postponement from the previously proposed date of January 2027, while definitively removing the requirement for e-reporting.

Form and details of the proposal

Mandatory e-invoicing in domestic B2B transactions

From 1 January 2028 onwards, electronic invoicing will be mandatory for all business-to-business transactions in Slovenia. This obligation will apply to all business entities registered with the Slovenian Business Register, as well as to individuals carrying out business activities. Paper invoices will no longer be accepted for B2B transactions.

E-invoices must be structured XML documents that enable the automation of business processes; PDF files will not qualify as e-invoices. E-invoices will be exchanged through decentralised secure channels using one of the following methods:

In the local eSLOG format, the primary standard used for exchanging e-invoices, and already in use for B2G transactions; Or

in any syntax in line with the European Norm 16931;

or in any other standard, subject to mutual agreement between the trading parties on a contractual basis.

If the issuer and recipient use different e-invoice formats, the e-invoice must be converted by a registered service provider (“ponudnikov e-poti”, or loosely translated, e-route or e-path providers). E-invoices can be exchanged via such registered providers, the Peppol network, or a direct connection between the parties, provided both parties agree to this method. Additionally, the Finančna uprava Republike Slovenije (FURS), the national tax and customs authority, will offer a free application called miniBlagajna (operated by) to facilitate the exchange of e-invoices for small-volume taxpayers.

Businesses dealing with consumers will also be able to send e-invoices to their private contractors, provided that the recipient consents and a legible version of the e-invoice is delivered, e.g., in PDF or another image format. E-mail providers can be used for exchange only if the recipient is a consumer.

Mandatory e-reporting - initially planned, but ultimately abandoned

The Slovenian proposal initially included a broader scope for e-reporting, additionally encompassing cross-border transactions for Slovenian operators (both suppliers and buyers) and B2C invoices. However, the final version of the legislation that was enacted removes the requirement for e-reporting. This means that the CTC component has been taken out of the system. The law does not require reporting on exchanged e-invoices to the FURS.

True to the nature of the DCTCE model, the country also foresaw the involvement of e-invoicing service providers. Businesses would have been able to report or send their transactions either through their own software or with the help of these service providers, who would have been required to undergo an accreditation process to be listed in the official register maintained by the Slovenian Public Payments Administration, UJP (Uprava za javna plačila).

The abandonment of mandatory real-time e-reporting does not lessen the importance of preparing for mandatory e-invoicing compliance, which will still come into effect.

Ensuring e-invoicing compliance

The VAT in the Digital Age (ViDA) reform, which was finally approved by the EU Finance Ministers at the 11 March 2025 ECOFIN meeting, is inevitably leaving its mark on the e-invoicing and e-reporting legislation in supporting countries. From 1 January 2028, the mandatory exchange of e-invoices for all Slovenian business entities is a gradual preparation for the amendment of the directive, which regulates value-added tax in the digital age. According to this directive, the issuance and exchange of e-invoices for cross-border transactions between VAT payers will be compulsory from 1 July 2030.

Mandatory e-invoicing is fast becoming a reality not only for businesses in Slovenia, but all over the world.

To ensure that your business becomes and remains compliant, it is essential to partner with an e-invoicing provider that is compliant in multiple countries worldwide. At Banqup Group, we are tax compliant in over 60 countries globally, and this number is growing continually.

We work closely with you to create the ideal e-invoicing solution for your business, offering value-added benefits that make business transactions even easier.

Explore our compliant e-invoicing solution today and connect with our local team to learn more. To receive updates on mandates and industry shifts in a more timely manner, follow us on LinkedIn.